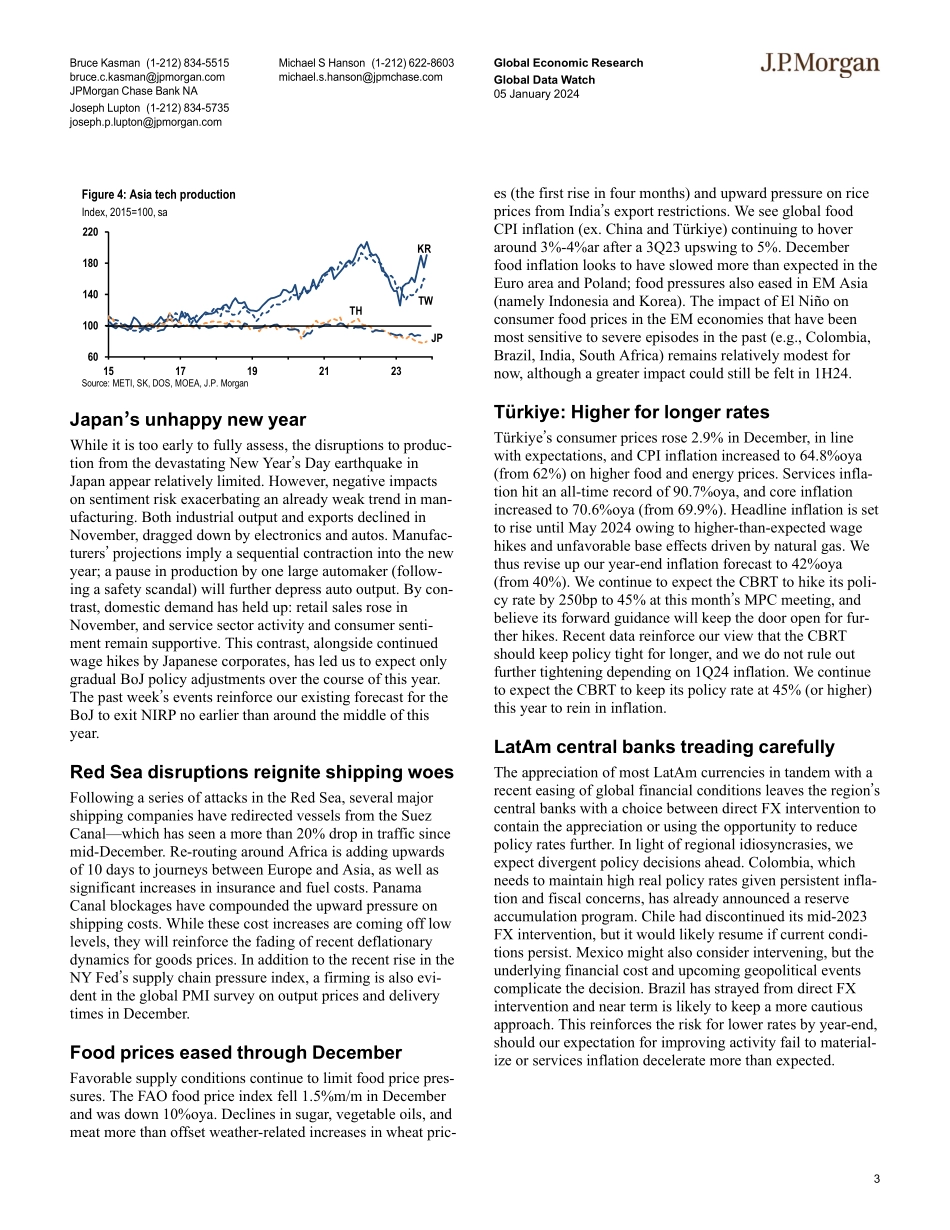

Global Economic Research05 January 2024J P M O R G A Nwww.jpmorganmarkets.comContentsNot so fast: Global core CPI to rise 3% in 1H24 12 Global Economic Outlook Summary4Global Central Bank Watch6Nowcast of global growth7Selected recent research from J.P. Morgan Economics9J.P. Morgan Market Watch10 Data Watches United States17Euro area22Japan27Canada29Mexico31Brazil33Argentina35Andeans37United Kingdom39Emerging Europe42South Africa47Australia and New Zealand48China, Hong Kong, and Taiwan50Korea53ASEAN55India58Asia Focus60 Regional Data Calendars61Economic and Policy ResearchBruce Kasman(1-212) 834-5515bruce.c.kasman@jpmorgan.comJoseph Lupton(1-212) 834-5735joseph.p.lupton@jpmorgan.comMichael S Hanson(1-212) 622-8603michael.s.hanson@jpmchase.comJPMorgan Chase Bank NAGlobal Data Watch•Disinflation not likely to be sufficient for rate cuts by March•PMIs underscore ongoing geographic and sectoral divergences•Geopolitics spark goods pricing inflation; Food prices falling•Next week: US Dec CPI (0.26% core); Nov IP (Ger, UK, Czk, Saf, Ind)It�s not soup yetCentral banks in the DM will not be ready to step back from their restrictive policy until they are convinced that core inflation rates are on a path to move sustainably below 3%. Inflation performance over the past six months has fueled optimism that we are on this path, with core inflation running at roughly 2%ar in both the US and the Euro area (Figure 1). This benign inflation backdrop has changed our thinking somewhat, as we have pulled forward our start of Fed easing and added another ECB cut this year. This comes alongside our recent upgrade to the likelihood of soft-landing. However, absent a growth threat, our central view is that it will take more time for central banks to reach this conclusion and look to midyear as the most likely time for DM central bank easing to begin (Figure 2). It is natural to extrapolate the sharp and broad-based slide in global core CPI inflation over the past six months. But as we highlighted this week, the primary driver of this move—goods price deflation—looks to be abating. Combining this with fading technical distortions, we expect Euro area core inflation to rebound to a 3%ar in 1H24. In the US, where core CPI inflation is running a percentage point higher than core PCE inflation, fading goods price deflation should offset an expected moderation in shelter inflation, keeping core CPI inflation stable at 3%ar. The recent weakness in “supercore� PCE service price inflation is harder to assess. But with non-market prices playing an important role in its slide and the CPI counterpart much firmer, the Fed is likely to view the slide cautiously. This week�s FOMC minutes suggest two judgments are important in a Fed forecast for 75bp of easing this year. First, “participants judged that the current stance of monetary policy was restrictive and appeared to be restraini...