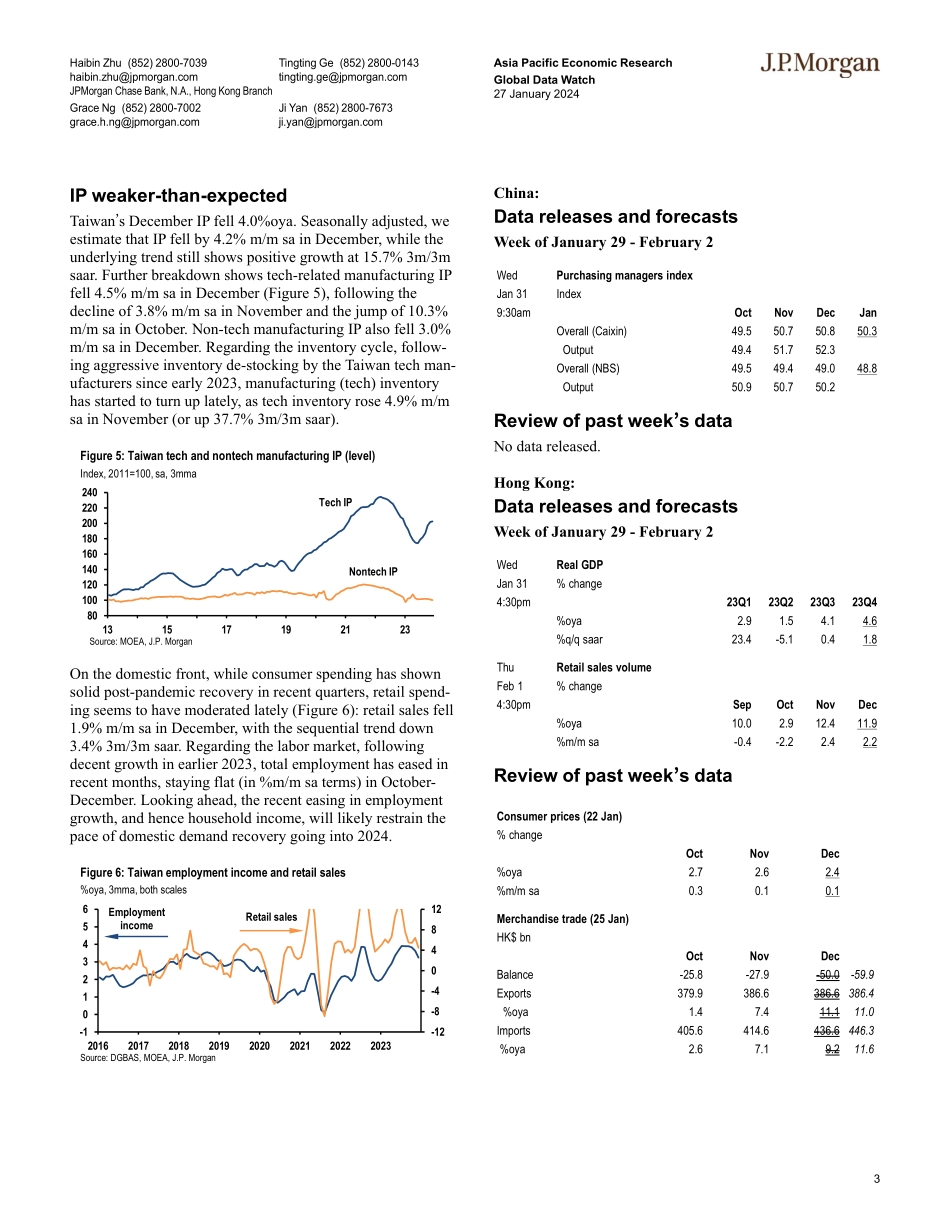

1Haibin Zhu (852) 2800-7039haibin.zhu@jpmorgan.comJPMorgan Chase Bank, N.A., Hong Kong BranchGrace Ng (852) 2800-7002grace.h.ng@jpmorgan.comTingting Ge (852) 2800-0143tingting.ge@jpmorgan.comJi Yan (852) 2800-7673ji.yan@jpmorgan.comAsia Pacific Economic ResearchGlobal Data Watch27 January 2024J P M O R G A Nimplies a more essential role of structural monetary policy instruments in the PBOC�s policy operation, compared to aggregate quantitative (e.g. universal RRR) or price-based (e.g. policy rate) policy instruments. In our baseline forecast, we have assumed a 1-trillion yuan package funded by PSL to support public housing and urban village developments, which has been echoed by the 350bn yuan net PSL injection in December. We also look for an expansion of re-lending facility to support debt restructuring as part of local governments� hidden debt resolution. These quasi-fiscal measures are targeted at addressing imminent vulnerabilities in the economy and financial system, and play an important role in our relatively constructive view on the Chinese economy in 2024. The announcement of further low-ering the re-lending and rediscount rates will further lower the funding cost for relevant sectors, including SMEs and rural development. Following the announcement, we remove our 2Q RRR cut forecast, but retain the 25bp RRR cut forecast for 4Q. This is not necessarily a high conviction call as the PBOC could expand medium-term liquidity injection through MLF opera-tion. On the policy rate front, we maintain our forecast for two rate cuts this year, 10bp each in 1Q and 3Q. Instead of more aggressive rate cuts anticipated by the market, we hold the view that the PBOC will continue to face multiple trade-offs in its policy rate decisions. Supportive factors include 1) deflation pressure, 2) reducing debt repayment burden, 3) mitigated pressure from currency depreciation and capital outflows, and 4) structural decline in natural interest rates, while constraints come from 1) limited room for monetary easing, 2) constraints in the banking sector (NIM compres-sion and capital adequacy pressure) and 3) debate on policy effectiveness. At the press conference, Governor Pan men-tioned the need to maintain a reasonable real interest rate lev-el in a forward-looking manner, to match the demand of sup-porting potential economic growth. We think the most macro and growth relevant indicator is TSF growth. Governor Pan reiterated that TSF and money supply growth should be in line with economic growth and inflation targets. We maintain our forecast for stable TSF growth at 9.5% this year, leaving credit impulse averaging at 5.0%pts (flat as 2023). Hong Kong: CPI inflation fellHong Kong�s headline CPI inflation fell to 2.4%oya in December, compared to 2.6%oya in November (Figure 2). Seasonally adjusted, headline CPI rose 0.1%m/m sa in December, adding to the 0.1%m/m s...